AI Generated image: Feature Normalization & Cost Optimization

This project explores the foundational concepts of machine learning by diving into feature normalization and cost optimization using linear regression techniques.

This project explores the application of linear regression using machine learning techniques. In this projects we are going use Linear regression Cost function convergence. This technique is practically applied to predict the house price and many other fields.

Linear regression technique is used to determine the model relationship between a dependent variable (target) and one or more independent variables (predictors). It assumes a linear relationship between the input variables and the output variable.

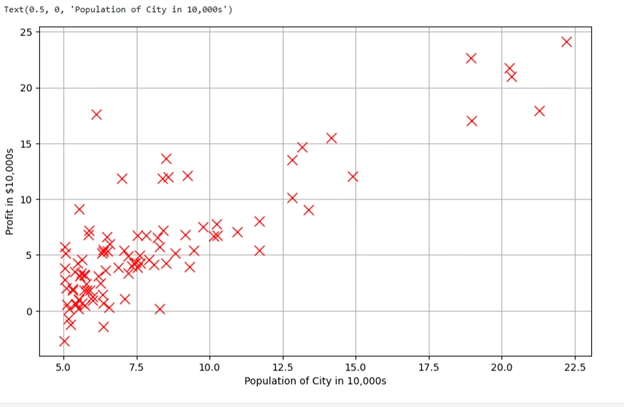

Before starting house price prediction let us plot an scattered graph to see how number of population effects on the profits. Here inputs x and y are converted into NumPy arrays.

%matplotlib inline

import numpy as np

import matplotlib.pyplot as plt

datafile = 'd:/mlprojects/data/ex1data1.txt'

cols = np.loadtxt(datafile,delimiter=',',usecols=(0,1),unpack=True) # Read in comma separated data

# Form the usual "X" matrix and "y" vector

X = np.transpose(np.array(cols[:-1]))

y = np.transpose(np.array(cols[-1:]))

m = y.size # Number of training examples

# Insert the usual column of 1's into the "X" matrix

X = np.insert(X,0,1,axis=1)

# Plot the data to see what it looks like

plt.figure(figsize=(10,6))

plt.plot(X[:,1],y[:,0],'rx',markersize=10)

plt.grid(True) # Always plot.grid true!

plt.ylabel('Profit in $10,000s')

plt.xlabel('Population of City in 10,000s')

Graph 1: Linear regression scatter graph

This is a scatter plot of the given dataset, where:

Gradient descent is an optimization algorithm used to minimize the cost function in machine learning models, particularly in linear regression. It iteratively adjusts the model parameters (theta) to find the best-fit line that minimizes the error between predicted and actual values.

We are using the following codes in cells of Jupyter Notebook:

iterations = 1500

alpha = 0.01

def h(theta,X): #Linear hypothesis function

return np.dot(X,theta)

def computeCost(mytheta,X,y): #Cost function

"""

theta_start is an n- dimensional vector of initial theta guess

X is matrix with n- columns and m- rows

y is a matrix with m- rows and 1 column

"""

#note to self: *.shape is (rows, columns)

# return float((1./(2*m)) * np.dot((h(mytheta,X)-y).T,(h(mytheta,X)-y)))

return float((1./(2*m)) * np.dot((h(mytheta, X) - y).T, (h(mytheta, X) - y)).item())

#Test that running computeCost with 0's as theta returns 32.07:

initial_theta = np.zeros((X.shape[1],1)) #(theta is a vector with n rows and 1 columns (if X has n features) )

print(computeCost(initial_theta,X,y))

After running above codes, results are:

32.072733877455676

We have used two important parameters:

We have defined the function h(theta, X) as:

def h(theta, X): # Linear hypothesis function

return np.dot(X, theta)

(h or hypothesis) by taking the dot product of

the feature matrix X and parameter vector theta.theta is set to all zeros.The function computeCost(mytheta, X, y) calculates the Mean Squared Error (MSE),

which quantifies how far the model’s predictions are from actual values.

def computeCost(mytheta, X, y): # Cost function

return float((1./(2*m)) * np.dot((h(mytheta, X) - y).T, (h(mytheta, X) - y)).item())

h(mytheta, X) - y calculates the difference between predicted and actual values.m is the number of training samples.

initial_theta = np.zeros((X.shape[1],1))

print(computeCost(initial_theta, X, y))

initial_theta is initialized with zeros.32.0727, meaning that with

untrained parameters (all zeros), the average squared error is 32.07.We run the following codes in the cells of Jupyter Notebook:

#Actual gradient descent minimizing routine

def descendGradient(X, theta_start=np.zeros(2)):

theta = theta_start

jvec = [] # Stores cost values for each iteration

thetahistory = [] # Stores theta updates for visualization

for _ in range(iterations): # Use range instead of xrange

tmptheta = theta.copy() # Explicitly copy theta

jvec.append(computeCost(theta, X, y))

thetahistory.append(list(theta[:, 0]))

for j in range(len(tmptheta)):

tmptheta[j] = theta[j] - (alpha / m) * np.sum((h(theta, X) - y) * np.array(X[:, j]).reshape(m, 1))

theta = tmptheta

return theta, thetahistory, jvec

#Actually run gradient descent to get the best-fit theta values

initial_theta = np.zeros((X.shape[1],1))

theta, thetahistory, jvec = descendGradient(X,initial_theta)

#Plot the convergence of the cost function

def plotConvergence(jvec):

plt.figure(figsize=(10,6))

plt.plot(range(len(jvec)),jvec,'bo')

plt.grid(True)

plt.title("Convergence of Cost Function")

plt.xlabel("Iteration number")

plt.ylabel("Cost function")

dummy = plt.xlim([-0.05*iterations,1.05*iterations])

#dummy = plt.ylim([4,8])

plotConvergence(jvec)

dummy = plt.ylim([4,7])

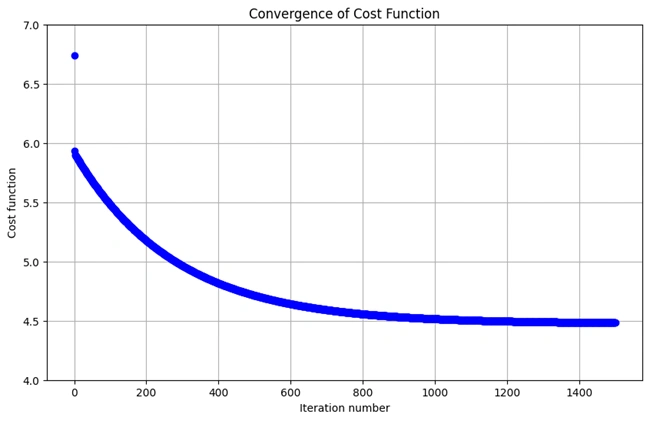

After running above codes, results are:

Graph 2: Showing how costs are decreasing with the increase of training iteration

We run the following codes in the cells of Jupyter Notebook:

#Plot the line on top of the data to ensure it looks correct

def myfit(xval):

return theta[0] + theta[1]*xval

plt.figure(figsize=(10,6))

plt.plot(X[:,1],y[:,0],'rx',markersize=10,label='Training Data')

#plt.plot(X[:,1],myfit(X[:,1]),'b-',label = 'Hypothesis: h(x) = %0.2f + %0.2fx'%(theta[0],theta[1]))

plt.plot(X[:,1], myfit(X[:,1]), 'b-',

label = 'Hypothesis: h(x) = %0.2f + %0.2fx' % (theta[0].item(), theta[1].item()))

plt.grid(True) #Always plot.grid true!

plt.ylabel('Profit in $10,000s')

plt.xlabel('Population of City in 10,000s')

plt.legend()

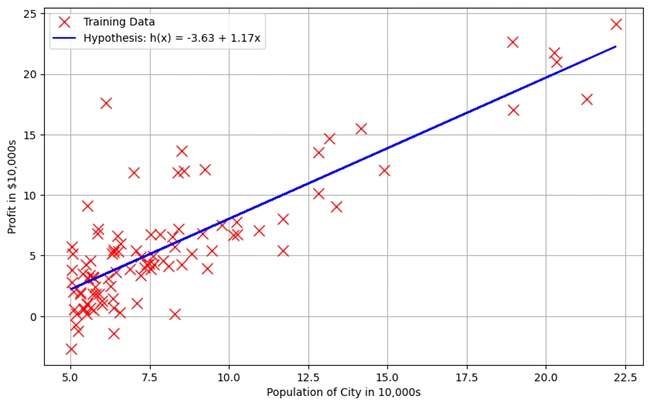

After running the above codes, the following graph is drawn:

Graph 3: Showing Linear Regression Best-Fit Line Over Training Data

This graph represents the fitted linear regression model plotted over the training data. The objective is to visualize how well the model captures the relationship between the population of a city and its profit.

We run the following codes in the cells of Jupyter Notebook:

#Import necessary matplotlib tools for 3d plots

from mpl_toolkits.mplot3d import axes3d, Axes3D

from matplotlib import cm

import itertools

fig = plt.figure(figsize=(12,12))

#ax = fig.gca(projection='3d')

ax = fig.add_subplot(111, projection='3d')

xvals = np.arange(-10,10,.5)

yvals = np.arange(-1,4,.1)

myxs, myys, myzs = [], [], []

for david in xvals:

for kaleko in yvals:

myxs.append(david)

myys.append(kaleko)

myzs.append(computeCost(np.array([[david], [kaleko]]),X,y))

scat = ax.scatter(myxs,myys,myzs,c=np.abs(myzs),cmap=plt.get_cmap('YlOrRd'))

plt.xlabel(r'$\theta_0$',fontsize=30)

plt.ylabel(r'$\theta_1$',fontsize=30)

plt.title('Cost (Minimization Path Shown in Blue)',fontsize=30)

plt.plot([x[0] for x in thetahistory],[x[1] for x in thetahistory],jvec,'bo-')

plt.show()

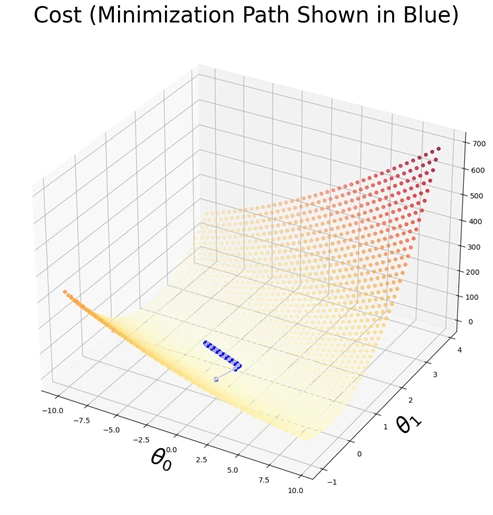

The following 3D Visualization Graph is generated:

Graph 4: 3D Visualization of the Cost function

This 3D plot represents the cost function \( J(θ) \) with respect to the parameters \( θ0 \)

and \( θ1 \). The surface demonstrates how the cost varies across different parameter values, with

the color intensity indicating the magnitude of the cost. The blue trajectory

illustrates the optimization path taken by the gradient descent algorithm as it

iteratively minimizes the cost, converging toward the optimal parameter values.

This graph provides a visual representation of the cost function landscape in a three-dimensional

space. The X and Y axes correspond to the parameter values \( θ0 \)and \( θ1 \), while the

Z-axis represents the computed cost \( J(θ) \). The scattered points on the surface denote

different cost values, color-coded to indicate their magnitude. The plotted blue path

shows the step-by-step progression of gradient descent as it moves towards the minimum cost.

This visualization is crucial for understanding how gradient descent optimizes the

parameters and ensures convergence towards the best-fit hypothesis.

We have run the following codes in a cell of Jupyter Notebook:

datafile = r'd:\mlprojects\data\ex1data2.txt'

#Read into the data file

cols = np.loadtxt(datafile,delimiter=',',usecols=(0,1,2),unpack=True) #Read in comma separated data

#Form the usual "X" matrix and "y" vector

X = np.transpose(np.array(cols[:-1]))

y = np.transpose(np.array(cols[-1:]))

m = y.size # number of training examples

#Insert the usual column of 1's into the "X" matrix

X = np.insert(X,0,1,axis=1)

#CODES IN CELL 11

#Quick visualize data

plt.grid(True)

plt.xlim([-100,5000])

dummy = plt.hist(X[:,0],label = 'col1')

dummy = plt.hist(X[:,1],label = 'col2')

dummy = plt.hist(X[:,2],label = 'col3')

plt.title('Clearly we need feature normalization.')

plt.xlabel('Column Value')

plt.ylabel('Counts')

dummy = plt.legend()

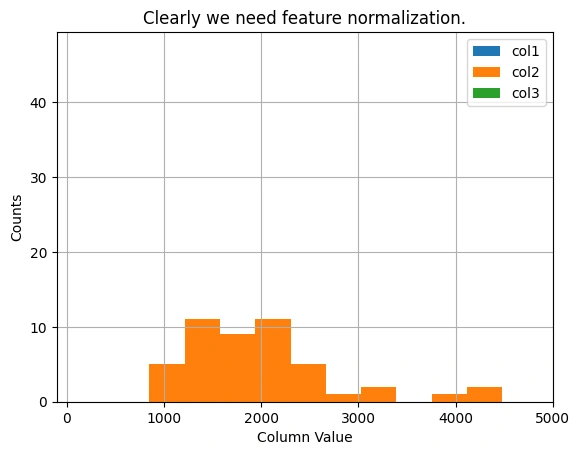

The following bar graphs are generated

Graph 5: Distribution of Feature Values Before Normalization

Feature scaling is crucial for gradient descent optimization. This histogram represents the dataset

before normalization.

The histogram visualizes the distribution of feature values in the dataset before

applying feature normalization. The three histograms correspond to different columns of the

dataset, showing a wide range of values. The need for feature scaling is evident, as the

features vary significantly in magnitude, which can impact the performance of

gradient descent.

This figure illustrates the distribution of dataset features before normalization. The X-axis

represents the feature values, while the Y-axis indicates the count of occurrences. The histograms

for different columns show that some feature values are much larger than others and all of them

having the same orange color.

Since gradient descent is sensitive to feature magnitudes, feature normalization is essential

to bring all features to a similar scale. This improves convergence speed and ensures that

the optimization algorithm progresses efficiently without being dominated by features with

larger numerical ranges.

Feature Normalization (Standardization or Min-Max Scaling) is required to bring all features to the same scale.

Feature normalization carried out by modifying the codes and running in Jupyter Notebook as:

#Feature normalizing the columns (subtract mean, divide by standard deviation)

#Store the mean and std for later use

#Note don't modify the original X matrix, use a copy

stored_feature_means, stored_feature_stds = [], []

Xnorm = X.copy()

for icol in range(Xnorm.shape[1]):

stored_feature_means.append(np.mean(Xnorm[:,icol]))

stored_feature_stds.append(np.std(Xnorm[:,icol]))

#Skip the first column

if not icol: continue

#Faster to not recompute the mean and std again, just used stored values

Xnorm[:,icol] = (Xnorm[:,icol] - stored_feature_means[-1])/stored_feature_stds[-1]

#Quick visualize the feature-normalized data

plt.grid(True)

plt.xlim([-5,5])

dummy = plt.hist(Xnorm[:,0],label = 'col1')

dummy = plt.hist(Xnorm[:,1],label = 'col2')

dummy = plt.hist(Xnorm[:,2],label = 'col3')

plt.title('Feature Normalization Accomplished')

plt.xlabel('Column Value')

plt.ylabel('Counts')

dummy = plt.legend()

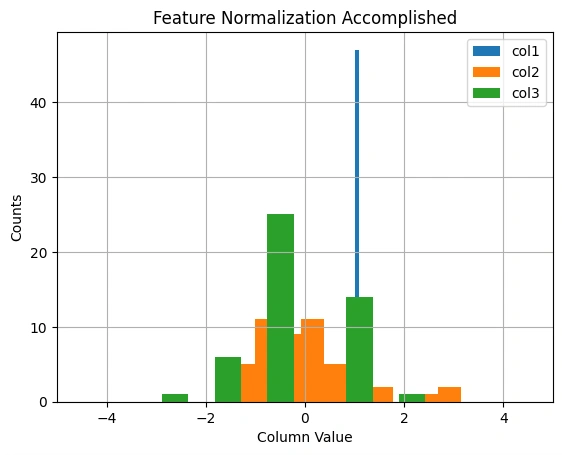

The following bar graphs are generated

Graph 6: Distribution of Features after Normalization

Feature normalization ensures a stable and efficient training process. The transformed

features are now on a similar scale.

This histogram illustrates the distribution of feature values after applying feature

normalization. The green, orange, and blue bars represent different features of the dataset.

The transformation scales the data to a common range, ensuring that all features have a

This histogram illustrates the distribution of feature values after applying feature normalization.

The green, orange, and blue bars represent different features of the dataset. The transformation

scales the data to a common range, ensuring that all features have a mean of zero and a

standard deviation of one, which improves the efficiency of gradient descent.mean of zero

and a standard deviation of one, which improves the efficiency of gradient descent.

Normalization Process: The code normalizes each column in the dataset X by

subtracting the column mean and dividing by the standard deviation. This process ensures

that each column has a mean of 0 and a standard deviation of 1.

Storage of Means and Stds: The code calculates the mean and standard deviation

for each column in X and stores them in stored_feature_means and stored_feature_stds

for later use.

Normalization: The Xnorm array stores the normalized values. Each column (except the first) in Xnorm is adjusted using the corresponding mean and standard deviation from stored_feature_means and stored_feature_stds.

Feature normalization is a crucial preprocessing step in machine learning, particularly for gradient descent optimization. This figure visualizes the effect of normalization on feature values.

This step ensures that features contribute equally to the learning process, preventing any single feature from dominating the optimization.

Feature normalization is critical in gradient descent, especially with multiple variables, because it ensures that all features (columns of Xnorm) are on a similar scale. Without normalization, the gradient steps could be uneven or "overflow" could occur during multiplication, making the algorithm fail.

Codes for convergence:

#Run gradient descent with multiple variables, initial theta still set to zeros

#(Note! This doesn't work unless we feature normalize! "overflow encountered in multiply")

initial_theta = np.zeros((Xnorm.shape[1],1))

theta, thetahistory, jvec = descendGradient(Xnorm,initial_theta)

#Plot convergence of cost function:

plotConvergence(jvec)

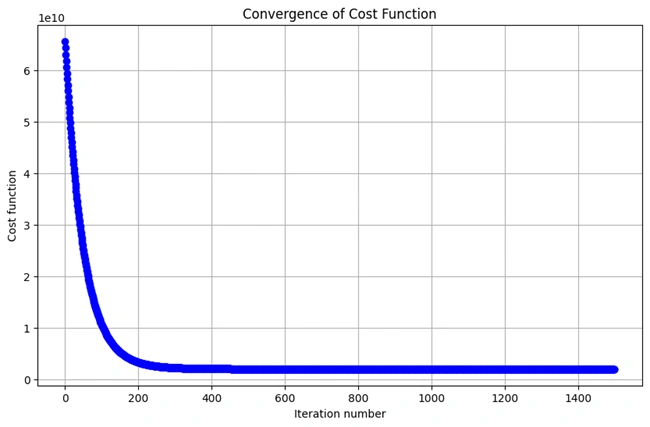

After running the codes the following graph is generated:

Graph 7: Convergence of the Cost Function in Multi-Variable Gradient Descent

Gradient descent minimizes the cost function iteratively. This graph shows the decrease in cost over time.

This plot illustrates the convergence behavior of the cost function over multiple iterations of gradient descent. The curved trajectory, resembling a right angle, indicates a rapid initial decrease in cost, followed by a gradual stabilization as the algorithm approaches the optimal parameters.

In multi-variable linear regression, gradient descent optimizes the cost function by iteratively updating model parameters. This figure visualizes the process:

This graph confirms that the gradient descent algorithm is functioning correctly, efficiently minimizing the cost function to improve model accuracy.

The bend line graph shows how the cost function decreases during the gradient descent process. Over time, as the algorithm converges, the cost approaches its minimum, which is where the model parameters (theta) are optimized.

I sincerely thank Prof. Andrew NG (DeepLearning.AI, Stanford University) for his inspiring courses that laid the foundation for this project.

www.HoqueAi.com

www.HoqueAi.com